Regulatory news

Q2 2026 enforcement update

Ben Parker

•

Chief Executive Officer & Founder

July 6, 2026

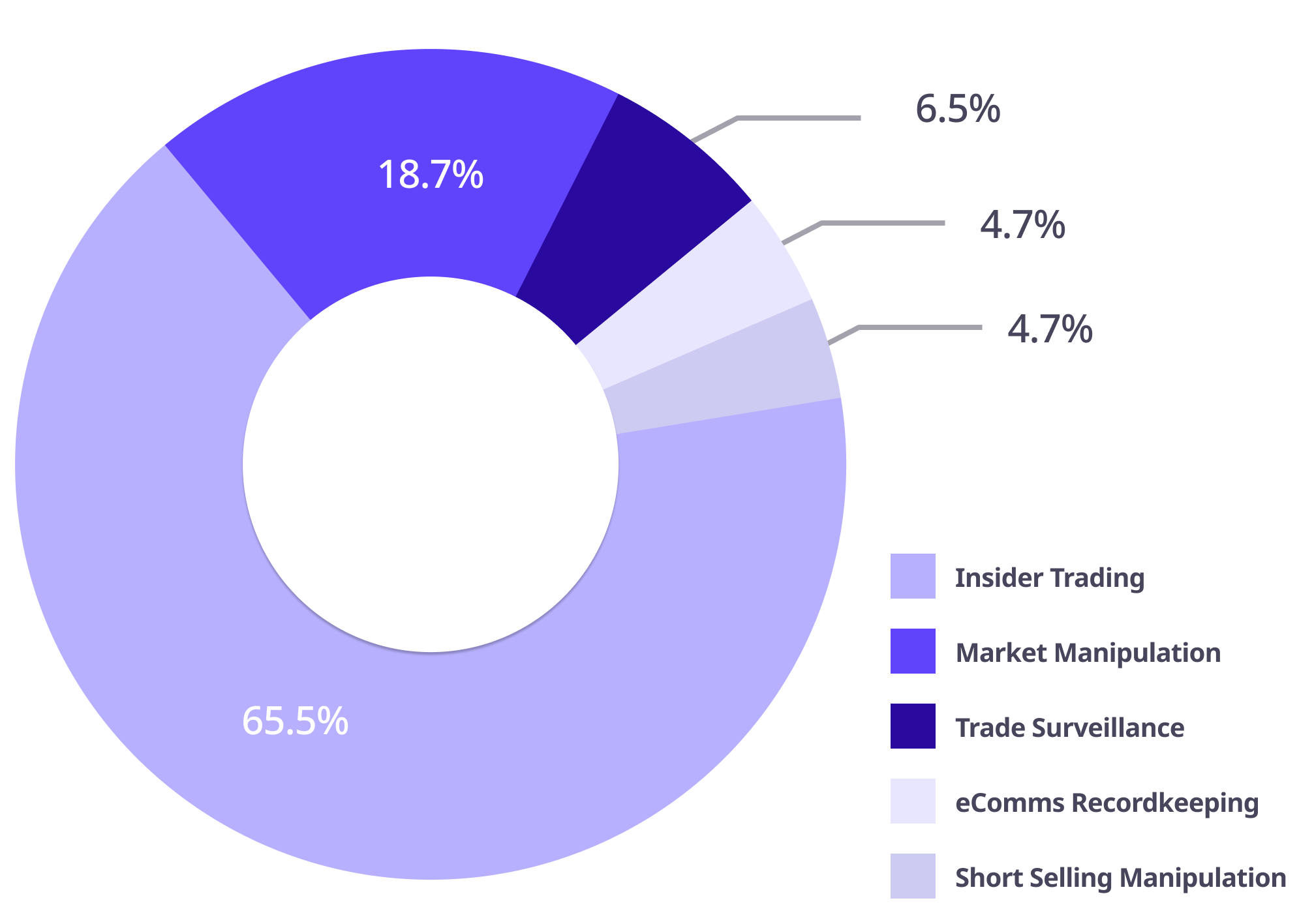

The second quarter of 2026 saw a high volume of enforcements in market abuse and trade surveillance, with a focus on proven cases of misconduct. Market manipulation and insider trading accounted for over 83% of tracked actions in Q2, but beneath the smaller overall value of fines are some of the most complex cases we've seen in years.

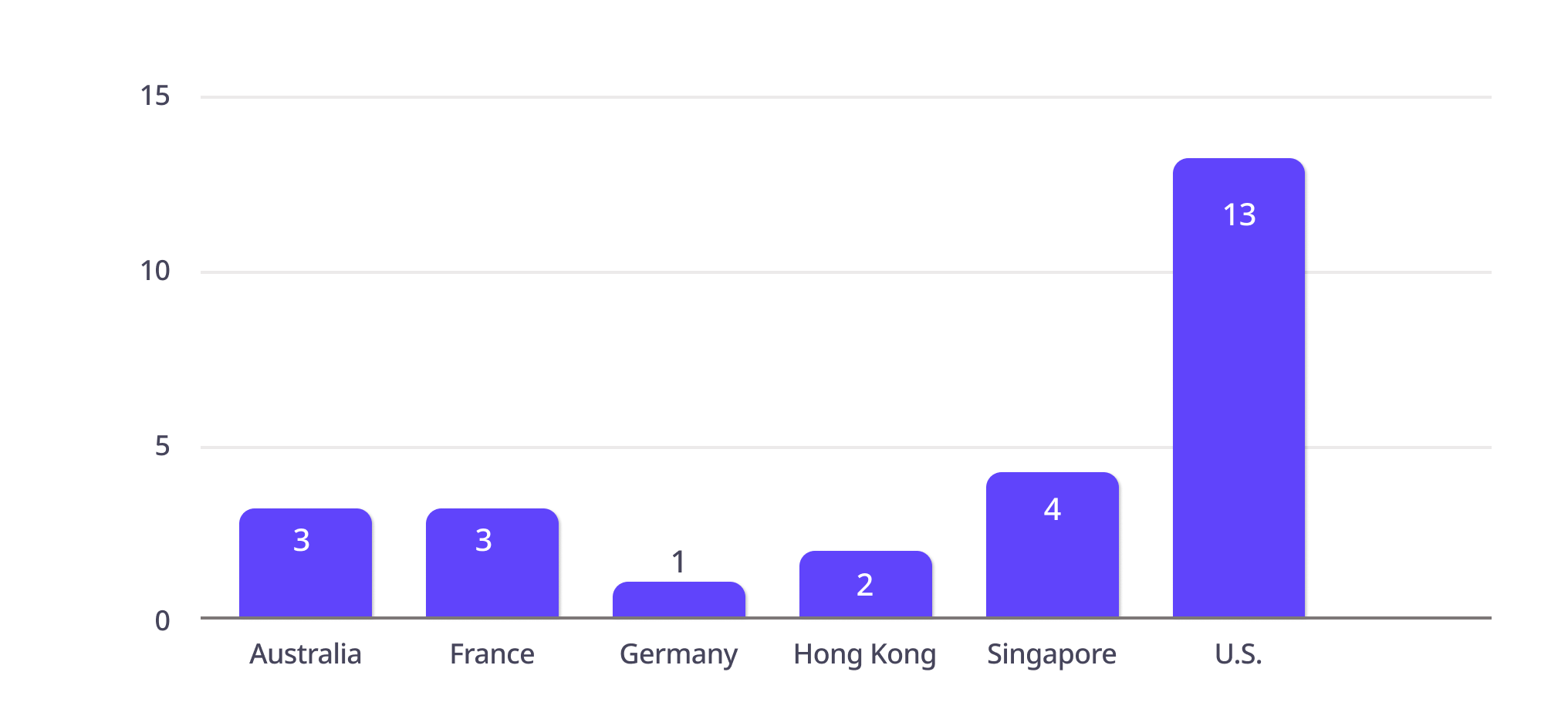

In Q2 2026, we saw 26 enforcement actions:

Across 6 jurisdictions:

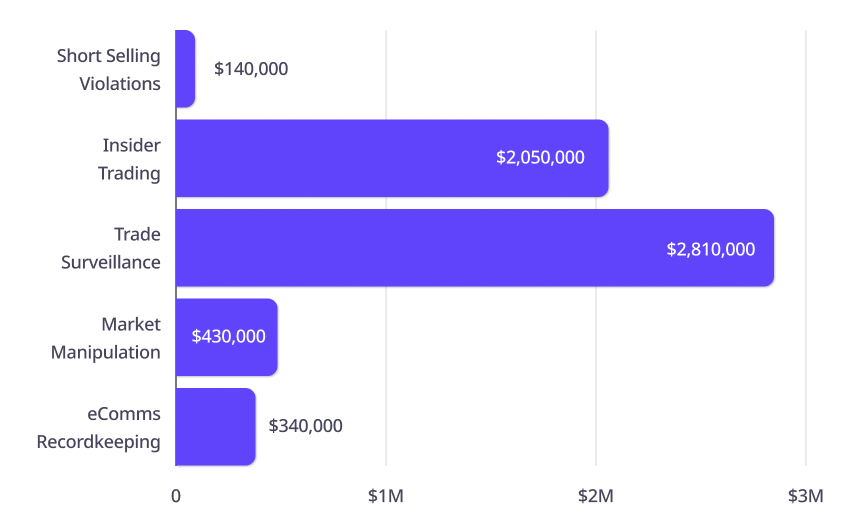

Totalling $5.7 million:

Insider trading dominated Q2 enforcement activity across every jurisdiction we track. The case count is high, and the geographic spread is broad.

The largest single fine came from BaFIN: a €1 million administrative penalty on flatexDEGIRO SE for not promptly disclosing inside information. The information in question concerned shortcomings identified during a BaFin special inspection of the firm's banking subsidiary, making this a case where the regulator effectively fined the firm for failing to disclose the findings of its own inspection. The delay and the decision to publish the information as a press release rather than an ad hoc disclosure formed the basis of the breach.

APAC was the most active region for insider trading enforcement this quarter, with material outcomes from MAS, ASIC, and the SFC.

Xie Jianfeng, then General Manager of Finance at Sasseur Commercial Management Group, traded Sasseur REIT units ahead of the release of the REIT's FY2020 financial results, earning profits of approximately S$223,000.

MAS also imposed a civil penalty on a doctor employed by a subsidiary of Singapore Medical Group, who purchased shares in the company after being approached by a potential acquirer and asked to sign an irrevocable undertaking, giving him advance knowledge of a privatisation that was not yet public. He traded days before the announcement.

The SFC secured the conviction of a film producer, chairman and controlling shareholder of Pegasus Entertainment for advising his sister to purchase shares in the company ahead of the disclosure of a significant transaction.

Former fund manager Rodney Forrest was re-sentenced for trading Platinum Asset Management shares ahead of a takeover offer. The Full Federal Court sentenced Forrest to five years and three months, one of the most significant sentences in Australian history for insider trading.

Two further cases produced guilty pleas during Q2: former Big Un CEO Richard Evans pleaded guilty to communicating inside information about the company's customer numbers and a major funding arrangement; and former Beacon Minerals project manager Alexander McCulloch pleaded guilty to procuring associates to trade while in possession of inside information about the company's gold exploration programme.

The largest and most structurally complex insider trading case of Q2 is making headlines ahead of a final verdict. The case centres on a decade-long tipping scheme orchestrated by two M&A lawyers who exploited their access to confidential deal files at four global law firms to trade ahead of more than twelve corporate transactions.

The architecture of the network is staggering.

The two M&A lawyers did not trade for themselves. They built a layered “tipping chain”, recruiting a third attorney to supply additional deal intelligence and then distributing tips through a series of middlemen, each of whom recruited further traders, predominantly from within tight social and family networks in Florida and New York.

The scheme ran on kickbacks: traders paid a percentage of their profits back up the chain, with cash payments, Zelle transfers, and in-person deliveries all documented in the complaint. The network communicated in code, using terms like "flights", "learning", and "rabbi's surgery" to refer to deals and announcement dates, and at times relied on prepaid phones to reduce the risk of detection.

The total profits alleged across 21 named defendants run to several million dollars. This will be one of the defining insider trading cases of the decade when it reaches its conclusion. We’ll be watching out for the first guilty pleas or settlements in Q3 and Q4 2026.

This case is a working illustration of how organised crime groups operate in financial markets and a stress test for the surveillance frameworks meant to catch them:

Last quarter, we said direct regulatory enforcement from the CFTC was “on the horizon”. Q2 confirmed it.

The CFTC has filed complaints against two individuals trading on Polymarket: a US Army service member alleged to have used classified government intelligence about a military operation, and a Google software engineer alleged to have traded Year in Search contracts using advance knowledge of confidential search data. Combined illicit profits: approximately $1.6 million. These are the CFTC's first-ever enforcement actions involving insider trading on prediction market event contracts.

Looking across the six actions, the deficiencies cluster into a few clear, recurring patterns.

At the start of the year, we predicted proportionality would increasingly define global enforcement, with regulators adopting a dual-track model: resolving minor breaches quickly to maintain market hygiene, while reserving resources for the complex, high-impact cases that deliver meaningful deterrence. H1 broadly supports that.

This quarter's trade surveillance actions make the point. Great Point at $250k, Instinet at $170k, Blue Ocean at $550k, Pictet at $610k, Bourse Direct at €850k, Impression at HK$2m: real deficiencies, priced modestly, resolved without protracted proceedings. Set against Q1's anchor, Canaccord at $40m combined, that's an order of magnitude difference and it tells us what regulators are actually pricing.

Culpability (negligence → wilfulness) is about intent.

Canaccord's failures were wilful. Staff deliberately manipulated surveillance filters to exclude over 99.99% of low-priced trades from review, then falsified records to mislead FINRA. Combined with a near-decade duration, 160+ unfiled SARs, and real investor harm through pump-and-dump schemes, this sits in an entirely different category from the honest-but-inadequate gaps seen in Q2.

Time (self-report early → conceal for years) is about your response.

Self-reporting and industry-identified suspicion draw explicit regulatory credit; failing to notice, or noticing and staying silent, is what escalates the eventual penalty.

We expect two things.

First, more actions against individuals in proven cases of misconduct. Regulators have invested heavily in their own data and analytics capabilities, and that investment is now bearing fruit; the SEC's 21-defendant insider trading network is exactly the kind of complex, multi-party scheme that only a sustained, intelligence-led investigation can unpick.

Second, on the institutional side, a return of the headline fine. The largest cases are the slowest to conclude; a complex, multi-party investigation can take years to move from opening to settlement. The relative quiet on institutional fines this quarter is better read as a function of where those cases sit in the pipeline than as any softening of intent. As the investigations regulators have been visibly resourcing reach their conclusions, we expect the headline penalties to follow in the second half of the year and beyond.