Regulatory news

Q1 2026 enforcement update: New risks emerging, familiar failures persist

Ben Parker

•

Chief Executive Officer & Founder

April 15, 2026

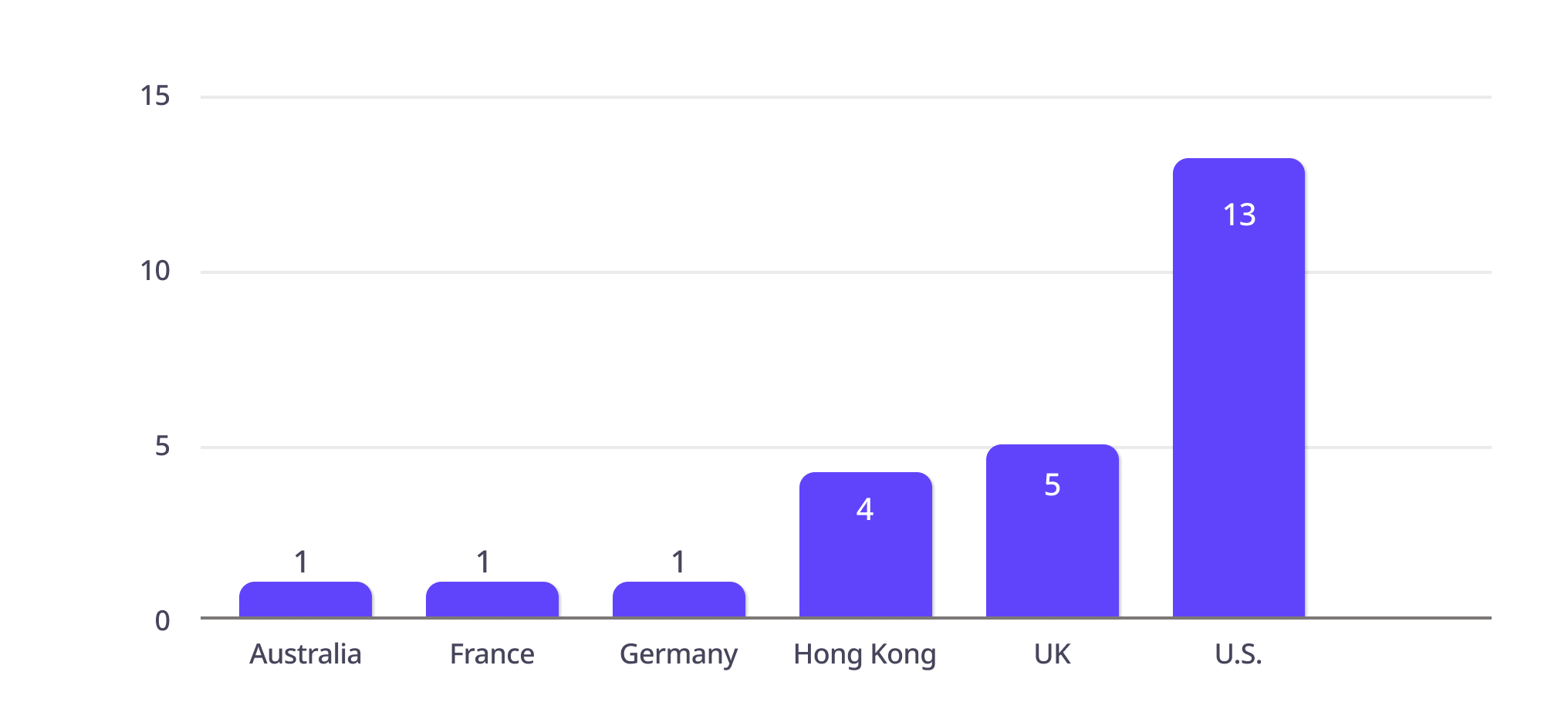

In Q1 2026, we saw 25 enforcement actions across 6 jurisdictions totalling $65m.

In Q1 2026, we saw 25 enforcement actions:

Across 6 jursidictions:

Totalling $65 million:

Our recent research identified prediction markets as an emerging area of market abuse risk. That thesis is now beginning to materialise. In Q1 2026, we saw the first clear cases of misconduct, with two enforcement actions tied directly to prediction market trading.

Both cases took place on the platform Kalshi. The individuals involved received financial sanctions and were suspended from direct or indirect access to the exchange. One case involved a political candidate trading on their own candidacy – a clear conflict with direct influence over the outcome. The other involved an individual trading on a prediction market linked to a YouTube channel while having an employment relationship with the subject of the contract, and therefore access to non-public information.

In our report, we pointed to insider-style advantages and emerging evidence of behaviours such as wash trading. At the time, these risks were largely theoretical, albeit supported by data and strong indicators. These cases mark a shift from plausible risk to proven misconduct.

It’s also notable that enforcement action was taken by the exchange itself. However, the CFTC quickly reinforced its position, stating that while Kalshi handled these cases internally, it retains full authority to police misconduct across designated contract markets.

This is being used as a deterrent, and the CFTC is watching closely. We expect two developments to emerge:

A $40 million combined penalty against Canaccord Genuity (split evenly between the SEC and FINRA) is highly relevant for firms managing market conduct risk. At its core, the case highlights how market abuse risk is sometimes understood and operationalised within the broader AML framework.

Canaccord’s process was straightforward on paper: trading activity is monitored, suspicious patterns are flagged, compliance investigates, and, where warranted, a SAR is filed. However, Canaccord failed in execution.

At the detection layer (trade surveillance)

At the escalation layer (AML governance)

Suspicious trading was either not captured, not reviewed, or not properly escalated resulting in approximately 150 SARs not being filed.

AML and market abuse surveillance are not separate controls, they are different regulatory lenses applied to the same trading behaviour. What matters is that suspicious trading is identified, investigated, and escalated appropriately. Where that chain breaks down, firms face enforcement, regardless of whether the breach is framed as AML or market abuse.

The Canaccord penalty highlights breakdowns across the full control chain. Similar themes emerge in the $7 million FINRA action against Credit Suisse, where large volumes of trade and order data were not captured in surveillance systems at all, preventing the detection of potentially manipulative and insider trading activity.

Across these cases, the root causes are consistent with those we called out in our research report: gaps in data capture, ineffective system configuration, poor integration following system changes, and weak governance over surveillance processes. Surveillance frameworks must work in practice, and we expect this to be a continued area of regulatory scrutiny throughout 2026.

While much of this quarter’s enforcement highlights persistent control failures, it’s equally important to recognise where frameworks are working as intended.

Kalshi’s response is one example – the exchange identified misconduct, took action, and enforced its own rules – demonstrating how effective surveillance can operate in practice, even in newer and less mature markets.

We see a similar dynamic in the UK. In two insider dealing cases, the Financial Conduct Authority explicitly referenced the “vital role of industry in uncovering market abuse”, with suspicious trading in both instances initially identified through STORs.

Effective surveillance is not defined by system sophistication, but by outcomes; specifically, whether those systems successfully detect and escalate genuinely suspicious behaviour. Where firms’ frameworks are functioning as designed, STORs remain one of the most direct and effective mechanisms for uncovering market abuse.