Trade surveillance

2025 market abuse and trade surveillance roundup: Investment managers

Ben Parker

•

Chief Executive Officer & Founder

April 27, 2026

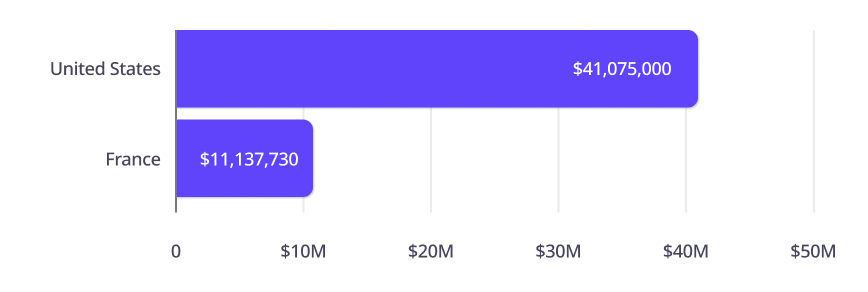

In 2025, global investment managers were the subject of $52 million in fines, with enforcement concentrated in a small number of high-impact cases.

Investment managers are inherently information-rich actors, operating close to corporate events, capital market activity, and critical investment decision-making.

They manage and transact significant volumes of financial assets on behalf of both institutional and individual clients. With constant pressure to deliver superior performance, the risk of misconduct is ever-present.

Our latest global report, Global Trends in Market Abuse and Trade Surveillance 2026, showed investment managers were the subject of $52 million in fines in 2025, with enforcement concentrated in a small number of high-impact cases.

In this blog, we unpack the drivers behind those fines, explore the structural challenges investment managers continue to face, and assess current maturity levels in adopting AI for trade and eComms surveillance.

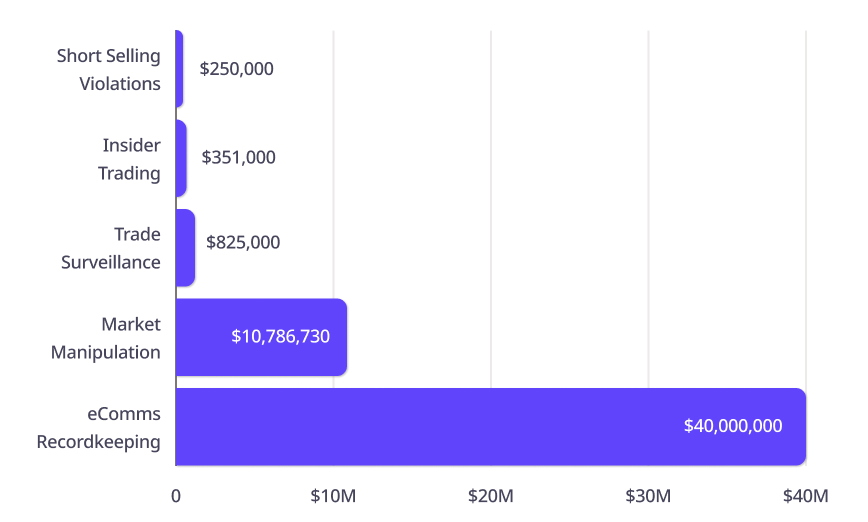

Enforcement activity in 2025 was highly concentrated, not just geographically, but also in terms of the types of market abuse failures.

While we observed enforcement across all major top-level typologies, the overwhelming majority (~97%) of fine value was driven by a narrow set of deficiencies. eComms recordkeeping failures accounted for ~76%, and a single, significant market manipulation case concluded by France’s AMF, representing ~11% of enforcement value.

Nine investment managers were swept up in the tail end of the SEC’s multi-year crackdown on eComms surveillance at the start of 2025. These cases exposed the same pervasive weaknesses that had defined earlier enforcement actions.

Firms were responding to SEC subpoenas while missing large volumes of relevant communications, a failure that, as noted by the regulator, “may have impacted the Commission’s ability to carry out its regulatory functions.” This goes to the heart of why penalties have remained significant, as failures directly undermine market oversight.

US-based fund, EcoR1 Capital, was fined €10 million by the AMF for cross-market manipulation.

The misconduct centred on Innate Pharma, primarily listed on Euronext Paris, which launched a Nasdaq ADS offering in 2019. Importantly, the ADS subscription price was mechanically linked to the five-day average closing stock price in Paris.

During this pricing window, EcoR1 sold aggressively into the close on Euronext Paris, depressing the reference price. This, in turn, lowered the ADS subscription price in the US, allowing the fund to acquire shares at an artificially reduced cost.

Structural linkages between markets can be deliberately exploited, making this form of abuse inherently difficult to detect. Firms rarely have full visibility across venues, limiting their ability to identify these patterns in isolation. We have observed a more coordinated, ecosystem-wide approach emerging, with firms continuing to enhance their controls and regulators stepping up to close the gaps, investing in advanced analytics such as network analysis and cross-asset visualisation.

Our own survey findings, conducted in January 2026, reinforce what we see in the enforcement data.

35% of investment managers say cross-product and cross-venue manipulation is keeping them up at night, while 42% struggle to integrate trade and eComms surveillance. These responses were both the highest recorded scores across all firm types surveyed as part of the research.

These align with the areas regulators are probing, and firms clearly lack confidence in the effectiveness of their controls.

Investment managers lag some peers in fully operationalising AI as part of their trade surveillance strategies. Just 19% of asset and wealth managers and 14% of fund managers report full deployment of AI across surveillance functions, compared to 21% of broking firms, for example.

This is partially offset by strong forward intent, particularly among asset and wealth managers. 32% report plans to deploy AI-enhanced trade surveillance processes within the next 12–24 months, the highest of any sector, compared to 27% in broking and just 15% in banking. Fund managers are slightly more muted at 23%, reinforcing the divide within the investment management segment itself.

The sector is in transition but not moving in lockstep. Asset and wealth managers appear further ahead in terms of their technology adoption, with clearer deployment roadmaps and stronger momentum, while fund managers lag, with a greater proportion still in exploratory phases.

In terms of how firms see AI having the greatest impact on their regulatory processes, the standout use case is analyst support. 57% of investment managers rank “copilot” capabilities among the most valuable applications of AI, compared to just 34% across other sectors.

The divergence from other firm types is notable. In segments such as broker-dealers, where AI adoption is more mature, analyst support tends to rank lower relative to more advanced use cases like anomaly detection and alert triage. This may reflect a deliberate prioritisation of copilot capabilities, or point to earlier-stage adoption and a more cautious approach to automation – only 36% of investment managers prioritise automating low-risk alert closure, versus 49% across the market, and 52% highlight AI-driven risk scoring compared to 58% elsewhere.

Investment managers lag behind peers in applying AI in eComms context and intent analysis (38% vs 41%). Enforcement data would suggest that foundational challenges around data capture and governance may still be limiting the effective deployment of more advanced AI capabilities in this area.

For more information on the regulatory challenges facing investment managers and how eflow’s technology can help firms to overcome them, visit our dedicated resources for asset and wealth managers, fund managers, and investment banks.